Many people have asked me how do they start investing? There are so many ways and so many techniques to investing that it makes a lot of people confuse. Do we look at charts? Do we use financial ratios? How do we know which companies to invest in?

I too was confused about the whole world of investing many years back. It was until I discovered what investing is really about that this confusion begin to disappear. Its like I saw the light at the end of the tunnel. In this post, I'll share with you a method of investing using the top down approach. Before we begin, let's understand what investing is really about and clear some misconceptions about the stock market once and for all. This will help you in understanding the top down approach better.

Misconceptions on Investing

Over the years, I've realised one main thing which caused the confusion for investing. It is that we do not understand investing at a deeper level. You see, most of us want to invest because we want to make a profit or grow our wealth. This is not wrong but it is not entirely correct either. Most of us end up trading the stock market which is totally different from investing.

Trading makes the stock market look like a gambling den. We look at charts and buy low sell high. Most will end up buying high and selling low. The main purpose is to make a profit and make as much money as possible. Some people even use software to give them buy and sell signals which makes the whole thing purposeless. In the case of trading, the companies we buy and sell is just a name. We just look at numbers instead of the company itself. If we take away the name of the companies and replace it with football team names, it becomes sports betting. If we take away the name of the companies and replace it with horses name, it becomes horse betting.

Don't get me wrong. I'm not saying trading is bad and there are professional traders out there who are successful in their own way. But if you're thinking about investing, then invest with the right approach and it'll be much clearer for you.

What exactly is Investing?Investing is owning a part of a company. When a company is listed on the stock market, it becomes a public company. Investors who wish to own a part of that company may buy the shares of it through the stock exchange. When we own shares of a particular company, we are entitled to certain rights such as voting rights and we also get a portion of the income in the form of dividends. When the company grows, the value of our shares in that company increases as well. It becomes more valuable.

Credit: http://pixabay.com/en/analysis-pay-businessmen-meeting-680567/

Top Down Approach To InvestingNow, when we know that investing is owning a part of a company, we should really ask ourselves what do owners of a company really want? What do we as owners want to see for the company?

I'm sure most of us would know the answer to the above question. We want the company to make money and grow. This is the best way to get return on our money for investors like us. There are two main elements that move a stock price. One is earnings and the other is news.

Bearing in mind that what we really want for the company is to make profit, the top down approach will start making sense now. This approach takes into consideration of the whole macro economic conditions that is happening now and also would happen in the future.

How to use the Top Down approach in investing?

The first step to the top down approach is to understand the elements of the macro economy. Some of you may have studied economics in JC or University which will be useful for this approach. If you have zero knowledge of economics, do not worry. I'll list down some elements and examples here which will be simple for you to understand. Let's start!

CurrenciesEvery country has their own currency except for the countries in the European Union which uses the Euro. More often than not, companies would have their business operated in a few different countries. Take for example a local company, Breadtalk. Although this company is started and headquartered in Singapore, they have branched overseas to more 15 countries including China, Philippines, Vietnam, Hong Kong, Taiwan, Cambodia, Malaysia etc.

Credit: https://www.flickr.com/photos/epsos/8463683689

As Breadtalk's main HQ is still in Singapore, they report their financials in Singapore dollars as well. When currencies of other countries weaken, it does affect the revenue and profit of Breadtalk. Companies can limit their exposure to currency risk by hedging using currency swaps.

Currencies fluctuate mainly due to monetary policy changes which shifts the demand and supply of it. For example, when US embarked on its massive quantitative easing which in essence is the printing of more money, the US dollar depreciates in value. Similarly, when Japan also embarked on its massive QE known as Abenomics, the value of the Yen depreciated as well. From these news on policy changes, we can predict quite accurately the movement of a particular country's currency and make smarter investment decisions.

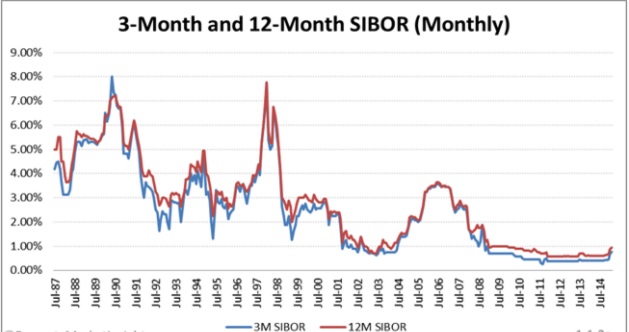

Interest RatesInterest rates drives the economy and affects a company's earnings. When a company has unsecured loans, they will be affected when interest rates rise. They will need more money to pay for the higher interest rates which in turn lower their profits.

Interest rates movement are mostly determined by the central bank of each individual country. The US central bank, called the federal reserve, often announce an increase or decrease in interest rates. Many countries practice an interest rate monetary policy including the European union and China. However, Singapore has an exchanged rate policy where our central bank strengthen or weaken the Sing dollar. Interest rates are increased when the economy is doing well and decreased when the economic situation is undesirable.

Commodities PricesCommodities prices such as oil, sugar, gas and other raw materials affect different companies and different sectors. When the price of oil dropped recently, there were concerns that those companies in the oil & gas sector would be affected. As such, this concern sent the prices of these companies down drastically. Similarly, when the cost of raw materials such as aluminium goes up, it can affect the margins of construction companies and they will earn a lower profit.

Commodities prices are mainly affected by the supply and demand of the economy. For oil prices, it is mostly controlled by the Organization Of Petroleum Exporting Countries (OPEC). OPEC is a cartel that aims to manage the supply of oil in an effort to set the price of oil on the world market, in order to avoid fluctuations that might affect the economies of both producing and purchasing countries. Simply said, when they pump in more oil into the economy, the prices of oil drop and when they withhold oil from the economy, the price of oil increases.

Picking Stocks using the Top Down ApproachThe above 3 elements are just some of the factors that can affect our investments. When picking stocks, we can look at the general outlook of the economy and determine which companies or industries will possibly do well in the future. Remember, if the companies do well, we get good returns on our investments while if the companies perform poorly, we can lose money.

Back in 2013 when I first looked at the economic situation in Japan, I thought it might be a good time to invest in the Japanese real estate market. The whole motivation behind investing in Japan's real estate is fundamentally due to economic reasons. Japanese prime minister Shinzō Abe has launched Abenomics which is a combination of measures such as quantitative easing (QE), increased public infrastructure spending and the devaluation of the Yen. All these stimulates growth which will increase asset prices. Investing in Japanese property may be a good choice if growth does set in and bring the Japanese economy out of a decade of deflationary economy.

True enough, real estate prices has been rising in Japan over the past 2 years. Rental yields have also gone up. As a result, the dividends I received from the Reits and business trusts I invested went up as well. It has given me stable income of about 7% consistently for the past 2 years. You can read about my investments in Japan

here.

Knowing how the macro economy functions can help us narrow down the potential areas we could invest in. This is just one of the strategy in stock picking. To learn more on how to pick stocks, you can read my previous post on stock picking

here.

Enjoyed my articles? You can Subscribe to SG Young Investment by Email or follow me on my Facebook page and get notified about new posts.Related Posts:

1.

Buying the company on the streets (Part 1) - Discovery stage2.

Company in focus - Breadtalk3.

Investing in Japan's Shopping Centres - Croesus Retail Trust Retail Investor Seminar