Interest rates are going up. This has been the concern for the past few months for many people. A rise in interest rates hurts borrowers and benefits savers. If you are a borrower, a rise in interest rates will really affect you. If you have existing loans such as car loans, housing loans and student loans, a rise in interest rates will mean you'll have to pay more every month to repay these loans.

If you have existing loans especially housing loans, here is some good news for you. There are ways to mitigate this rise in interest rate and reduce the impact it has on you to the lowest. In this post, I'll show you what the industry calls Fixed Deposit Home Rate. This is an alternative rate to SIBOR which I believe is much better for home loans. If you're on a SIBOR or other variable home loan packages, read on to find out more about this new rate which will be beneficial for you to refinance to.

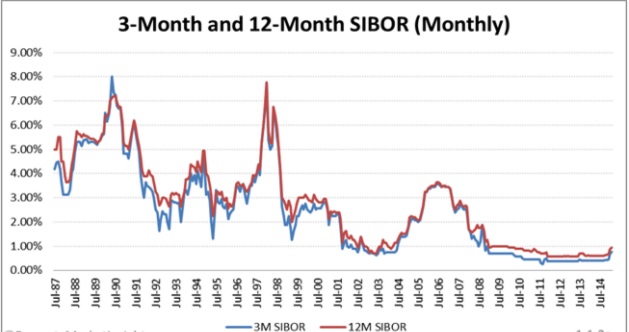

How Do We Know If Interest Rates Are Rising In Singapore?

The most widely used rate for interest rates here in Singapore is the SIBOR. It is called the Singapore Interbank Offer Rate, a rate which Singapore banks lend to each other. There is the 1 month SIBOR, 3 month SIBOR and the 12 month SIBOR. These rates are commonly used for housing loans when you loan from the bank on a variable rate package.

Currently, the 3 month SIBOR is about 1.1%. The highest 3 month SIBOR was 7.75% in January 1998 and the lowest was 0.25% in September 2011. From the chart below, SIBOR can really swing quite widely. It is really possible for SIBOR to increase back to the 2-3% mark.

When SIBOR increases by too much, those with housing loans will have to pay more for their instalments. For the past few months, I've been working closely with banks for my mortgage consultancy work. I've seen rates increase and also helped people refinance their home loans to better rates. There is an alternative rate to SIBOR which I think is a better choice for those with existing home loans. If you have existing home loans, listen to this carefully as it will definitely help you save more money in the long run.

Fixed Deposit Home Rate - The Alternative Interest Rate To SIBOR

In the past, there are only limited choices for home loans. People either choose the fixed rate packages or the floating rate packages pegged to SIBOR or the bank's board rate. For SIBOR, the rate is too volatile while the bank's board rate is not as transparent meaning the rate can change as and when the bank decides to change.

To safeguard ourselves against interest rates increase, we can choose the fixed rate packages but fixed rate packages are only available for 2 years to a maximum of 3 years currently. Thereafter, the rate will revert back to the variable package pegged to either SIBOR or bank's board rate again.

Now comes a new package called the fixed deposit home rate. This rate is pegged to a bank's fixed deposit rate where it is certainly less volatile than the SIBOR. Why the fixed deposit rate does not increase that much is because increasing this rate is a cost to the bank. Especially in Singapore where a lot of cash is parked in the fixed deposit accounts, banks have to think twice before increasing this rate.

From the past historical trend, the highest fixed deposit rate was around 0.875%-0.925% as compared to the highest rate of SIBOR at 7.75%. The fixed deposit rate can be either pegged to the 12 month, 18 month, 24 month or 36 month rate. Currently, only 2 banks in Singapore offer this home loan package which is pegged to the fixed deposit rate.

Refinancing to this rate would mean more stability for our monthly housing loan instalment and cost savings in the long run. To find out more about this rate or refinance your housing loans to this rate, you can email me at sgyi@homeloanwhiz.com.sg. I do not charge any fees for providing advice or refinancing your loans. This is a strictly complimentary service I offer to readers here.

Alternatively, fill in the contact form below for a free consultation and I'll get back to you shortly:

foxyform

No comments:

Post a Comment